After this post on my 8 (+1) credit cards (not click-bait, I really do own them all), you may be curious…

💳 Did I pick random cards to sign up? NO

💳 Do I pay my bills on time? YES

💳 Do I pay annual fees? NO

💳 Is my credit score terrible? NO

💳 Is this my best strategy? Hmm not really yet? 🤔

Let me share some of my #Tips

⛔️❗️Warning❗️⛔️

Before you start, you will need to make sure that you are in control of your spending and can pay your bills on time. Credit card interests and hefty (close to 30%) and you incur interests too if you repay the minimum sum only. It is advisable to start getting credit cards only if you are mindful of your spendings

…..alright, let’s get into it

1️⃣ Choose the right credit cards for yourself

Always remember these principles:

✨Credit card must follow your spending pattern, not the other way round

✨If the card has complicated rewards system and you don’t know how to make use of it, DO NOT get it. You won’t max it’s benefits anyway and will confuse you further

When I first apply for my credit card, I wasn’t sure what I would spend on. Moreover, I recently joined the workforce, and my spending power isn’t a lot.

Thus, I started to track my expenses daily, and try to categorise them based on the MCC codes that credit cards follow (i.e Dining, Retail etc).

From a few months of data, I noticed that I have:

💵 Wide range of spendings, mainly on dining and occasional shopping

💵 Many offline transactions instead of online

💵 Do not have consistently large spends on a certain category

💵 Huge wedding expenses and honeymoon in the coming years

Thus, I selected the cards base on my spending patterns. These are some criteria I listed:

🪙 No minimum spend

🪙 Has wide range of qualifying spends for both offline and online transactions

🪙 No Annual fee (or annual fee waive-able)

This is the most important step to as having a solid set of criteria determines the foundation to your strategy.

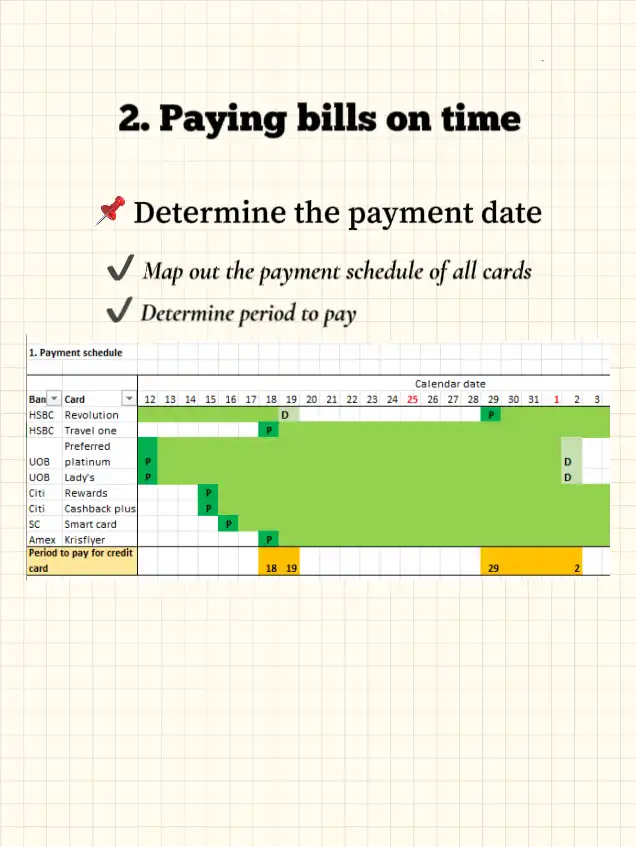

2️⃣ Paying bills on time by determining payment date

With many cards from different banks, there will be different payment schedule. It is not easy trying to remember the deadline especially if you have many cards.

Hence, I determined a date where the payment schedules of all the card overlaps, and make it a point to pay my bills at that date 🗓️

To visualise the period of payment, I lay out the periods on an excel and determine the time period to pay.

So far I’m lucky that the cards have pretty similar schedules (except HSBC Revo), and if you want to change your payment schedule, you can give the bank a call 📞

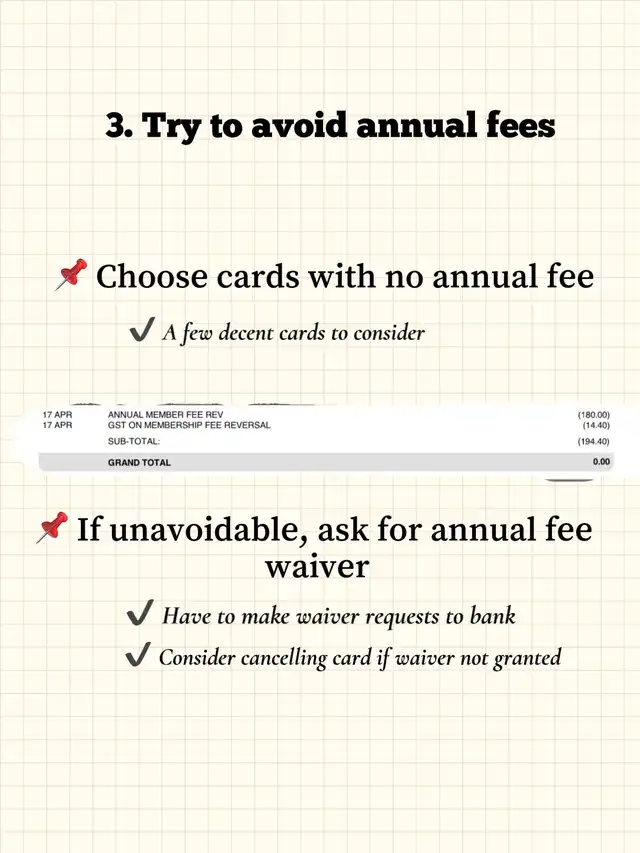

3️⃣ Waive off annual fee as much as possible

First, get a card with no annual fee required (i.e HSBC revolution, SC smart card). There are not much out there, but a few a pretty decent

If not possible, try to waive off the annual fee by sending in the request (or even calling) to the bank. Most cards comes with first year annual fee waived, so you would only need to do that the next year. If you pay your credit card bills on time, charge a good significant amount to it, the chances you will obtain waiver will be high.

If they don’t want to waive off or counter-offer with something not ideal, just cancel the card and move on to another one, so long the card is not beneficial. Remember that banks are competing for customers.

Banks may sometimes give you reward for paying their annual fee (i.e miles). You may want to analyse if it is worth to pay for the rewards before paying the annual fee (See: How to value miles)

4️⃣ Maintain a good credit score

I have a separate post that explains the credit report in detail

In essence, the key contributing factors are:

🔺Credit history

🔺Credit exposure

🔺Enquiries to your credit status

(Criteria taken from CBS credit report)

To maintain good credit score, remember these few points:

💯ALWAYS pay your bills on time

💯If you just started working, apply for easy to obtain cards first, and charge small amounts to the card and repay them on time. This will let you create a good payment record

💯Spread out your credit card application (to reduce number of enquiries in a short period of time), and apply for cards that you really need (see point 1️⃣)

💯Do not consistently max out your credit card, or use till your credit limit

5️⃣ Acknowledge and embrace changes

There will definitely be better cards coming up, and your spending patterns will definitely evolve in the future.

Thus, I would expect my credit card strategy to adapt to my changing needs. Having an open mind to constantly read up and fine running my credit card strategy will ensure that you are always maximising the benefits of your card.

Moreover, it takes time and effort to build a credit card strategy. Hence, it is important to be patient too, as you are building your army of cards and your credit scores

Do not be afraid of changes and embracing them along the way!

#AdultingWoes #Adulting101 #creditcards #financesg #financialplanning